Most new traders focus on direction. They ask whether a stock will go up or down. Professional traders focus on exposure. They ask how much they stand to gain or lose if price moves. Delta is the metric that answers that question. Before thinking about profit targets, before debating market direction, and before selecting strikes, understanding Delta allows a trader to quantify how sensitive their position is to price movement. Without that measurement, position sizing becomes guesswork.

At its most practical level, Delta estimates how much an option’s value will change if the underlying stock moves $1.

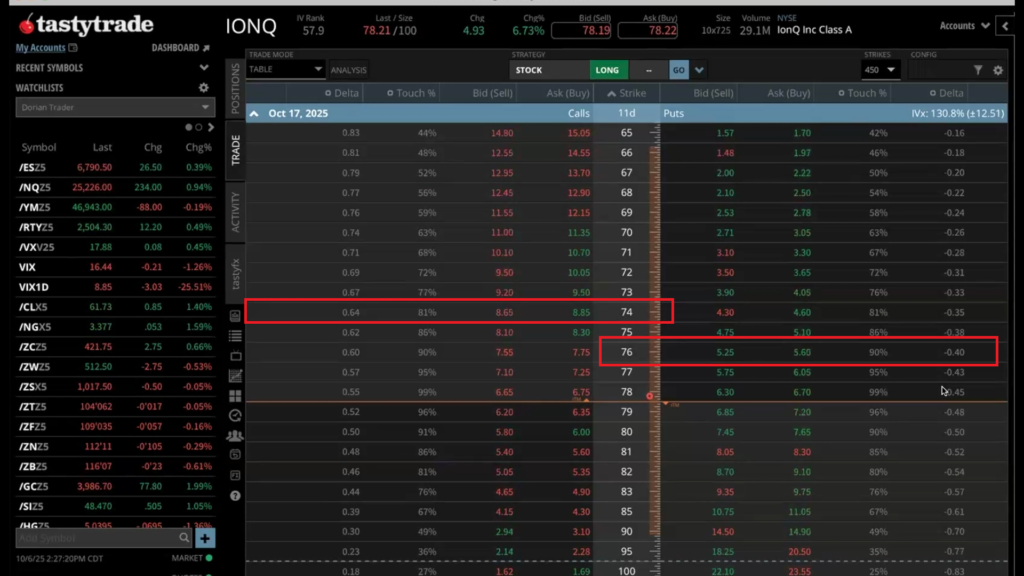

If an option carries a 0.64 Delta, it is expected to gain approximately $0.64 for every $1 move in the underlying. If it carries a -0.40 Delta, it is expected to gain approximately $0.40 if the stock drops $1.

The sign tells you direction. The number tells you magnitude.

However, this is not a fixed relationship. Delta shifts as price moves, as time decays, and as implied volatility expands or contracts. It represents current sensitivity — not a permanent rate of change.

Many traders think in terms of contracts. Experienced traders think in terms of Delta. One share of stock equals 1 Delta. That exposure does not change. Stock positions are static. Options are different. Their Delta changes daily.

If you purchase one call with a 0.50 Delta, you are controlling exposure similar to 50 shares of stock. Two contracts at 0.50 Delta equal roughly 100 shares of exposure. A single contract with 0.80 Delta behaves closer to 80 shares. When traders ignore this relationship, they often take on far more directional risk than intended.

At Dorian Trader, position size always begins with understanding total Delta exposure, not the number of contracts traded.

If you would like to better understand the true mechanics of Delta and how it applies to real trading decisions, watch the Dorian Trader video linked below:

Delta also provides a practical estimate of the probability that an option will expire in-the-money.

A 0.20 Delta suggests roughly a 20% probability of expiring ITM.

A 0.75 Delta suggests roughly a 75% probability of expiring ITM.

This is where strategic decisions differ between buyers and sellers.

Option buyers who choose extremely low Delta contracts are accepting low probability outcomes in exchange for lower cost. While this may appear attractive, the math does not favor repeated low-probability trades without exceptional timing.

Option sellers, on the other hand, frequently position themselves where probability favors them, often in the 0.10 to 0.20 Delta range and collecting premium with a statistical edge. However, probability is not protection. A high-probability trade still requires defined risk and disciplined management.

Delta is dynamic because options are nonlinear instruments. As price approaches a strike, Delta accelerates due to Gamma. As expiration approaches, sensitivity increases further, particularly for at-the-money contracts.

Implied volatility also affects Delta behavior. During volatility expansions, option premiums may increase even without large directional movement. During volatility contraction, gains from Delta can be partially offset. For this reason, Delta should never be viewed in isolation. It is a measurement within a broader risk framework.

A critical but often overlooked concept is the difference between expiring in-the-money and touching a strike before expiration. Market behavior suggests that the probability of touching a strike is frequently much higher than the probability of expiring there. An option with a 0.25 Delta may only have a 25% chance of expiring ITM, yet the likelihood of price reaching that strike at some point during the trade can be significantly greater.

This distinction reinforces the importance of active management. Waiting until expiration ignores how options actually trade throughout their lifecycle.

Delta should also be viewed at the portfolio level. Individual trades may appear balanced, but combined exposure can create unintended directional bias.

Professional traders monitor their net Delta across all positions to understand how a broad market move would affect their account. Some traders even compare exposure relative to market benchmarks such as SPY in order to measure how their portfolio responds to overall market movement rather than just single stocks. This broader view prevents overconcentration and improves consistency.

It defines how much exposure you carry. It approximates your probability. It translates options into stock equivalency.

When traders shift from asking “Will this work?” to asking “What is my Delta exposure?” they move from speculation toward structured risk management.

Long-term consistency in options trading does not come from forecasting every move correctly. It comes from understanding exposure, controlling position size, and aligning probability with disciplined execution. That process begins with Delta.

Ready to build your income strategy with expert support?

1. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.