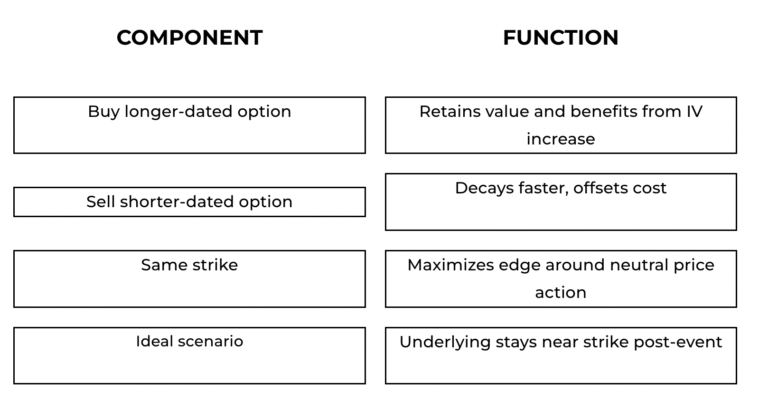

![]() Buy a longer-dated option

Buy a longer-dated option

![]() Sell a shorter-dated option

Sell a shorter-dated option

![]() Both at the same strike

Both at the same strike

![]() Earnings announcements

Earnings announcements

![]() CPI or jobs reports

CPI or jobs reports

![]() Federal Reserve meetings

Federal Reserve meetings

![]() Market environments where front-month IV is inflated

Market environments where front-month IV is inflated

![]() Directional move: If price moves sharply away from the strike, both legs may lose value

Directional move: If price moves sharply away from the strike, both legs may lose value![]() Volatility crush: If IV drops across both expirations, especially after earnings, the position may decline

Volatility crush: If IV drops across both expirations, especially after earnings, the position may decline![]() Gamma exposure: As the short option nears expiration, price swings can affect the trade more aggressively

Gamma exposure: As the short option nears expiration, price swings can affect the trade more aggressively